Health and Household Finance

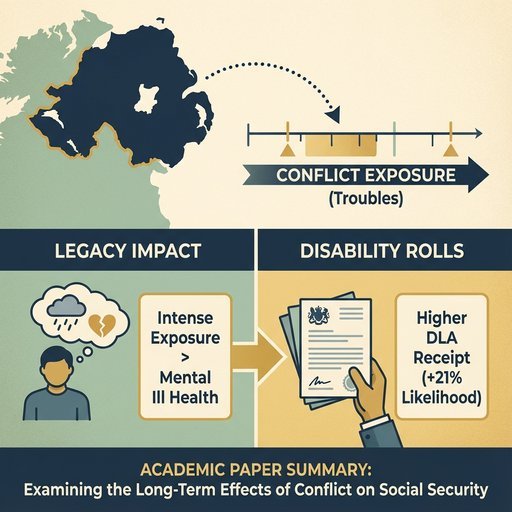

The legacy of the Northern Irish 'Troubles' on Disability Rolls

Social Science & Medicine, 2025

Anne Devlin; Declan French; Duncan McVicar

Disability benefit recipiency rates have been persistently higher in Northern Ireland (NI) than the rest of the UK for decades. Receipt of Disability Living Allowance (DLA), a social security payment designed to cover the additional costs of living with a disability, was proportionally around twice as high in NI compared to the rest of the UK at its 2016 peak. This paper uses data from the Northern Ireland Cohort of Longitudinal Ageing survey to examine whether one potential contributory factor, exposure to the conflict, can explain variations in DLA receipt among older working-age people in Northern Ireland. Conflict-related fatality rates at the area level are used to account for potential endogeneity in reporting past exposure to trauma. While most of the NI population in the age bracket examined (50-64 years) were exposed to the conflict in some way, more intense exposure to the conflict is found to increase the likelihood of DLA receipt by 21 percentage points. We also find a substantial impact on mental ill health. This research has significant policy ramifications both in NI but also across the UK at a time of particular interest in disability benefit receipt as well as contributing to the wider post-conflict literature.

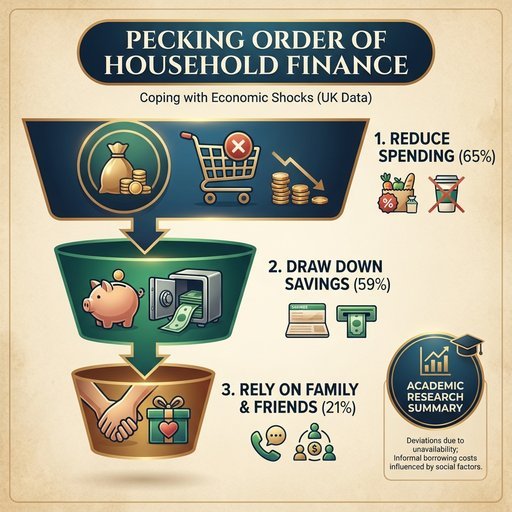

A pecking order of household finance

Oxford Economic Papers, 2025

Declan French

How do households cope with economic shocks? In this article, I provide empirical evidence and theoretical grounding for a pecking order of coping methods using data from the UK Understanding Society COVID-19 Study. I find that there is a typical household finance ordering of responses to income loss. Almost two-thirds (65 per cent) of households first reduce spending then these households typically proceed to draw down savings (59 per cent) and their most common next response is relying on family and friends (21 per cent). Deviations from this ordering occur because certain coping methods are of ten unavailable—those households not reducing spending are already struggling and those without savings have nothing to drawdown. Receiving financial assistance from family and friends is also more common than some authors suggest. Lastly, I find that the costs of informal borrowing are influenced by plausible social factors. My results are informative for policies to promote resilience during crises.

Transportation resilience under Covid-19 Uncertainty: A traffic severity analysis

Transportation Research Part A: Policy and Practice, 2024

Qiao Peng, Yassine Bakkar, Liangpeng Wu, Weilong Liu, Ruibing Kou, Kailong Liu

Transportation systems are critical lifelines and vulnerable to various disruptions, including unforeseen social events such as public health crises, and have far-reaching social impacts such as economic instability. This paper aims to determine the key factors influencing the severity of traffic accidents in four different stages during the pre- and the post Covid-19 pandemic in Illinois, USA. For this purpose, a Random Forest-based model is developed, which is combined with techniques of explainable machine learning. The results reveal that during the pandemic, human perceptual factors, notably increased air pressure, humidity and temperature, play an important role in accident severity. This suggests that alleviating driver anxiety, caused by these factors, may be more effective in curbing crash severity than conventional road condition improvements. Further analysis shows that the pandemic leads notable shifts in residents' daily travel time and accident-prone spatial segments, indicating the need for increased regulatory measures. Our findings provide new insights for policy makers seeking to improve transportation resilience during disruptive events.

Exploring household financial strain dynamics

International Review of Financial Analysis, 2023

Declan French

Rising energy and food prices are causing living standards to fall across Europe and straining household budgets. The longer-term outlook for households is unclear as the dynamics of financial strain are not well understood. We address four important research questions on financial strain dynamics by applying a dynamic random coefficients probit model with duration and occurrence dependence to De Nederlandsche Bank (DNB) Household Survey panel data. We find no evidence that households become habituated or sensitised to financial strain over time unlike in studies of responses to stress. Entry into household financial strain is less likely when the household can cope by increasing earnings from work or by borrowing from family and friends but not by the economically inactive entering employment. Our third result is that the persistence of financial strain can be explained by a mutually-enforcing negative cycle through worse health but not through marital conflict or more short-sighted and risk averse decision-making. Finally, we find that neither income or wealth shocks affect financial strain in contrast to other studies. Further research into understanding the experience of financial hardship is warranted in the light of the economic challenges caused by the current cost of living crisis.

From financial wealth shocks to ill-health: allostatic load and overload

Health Economics, 2023

Declan French

A number of studies have associated financial wealth changes with health-related outcomes arguing that the effect is due to psychological distress and is immediate. In this paper, I examine this relationship for cumulative shocks to the financial wealth of American retirees using the allostatic load model of pathways from stress to poor health. Wealth shocks are identified from Health and Retirement Study reports of stock ownership along with significant negative discontinuities in high-frequency S&P500 index data. I find that a one standard deviation increase in cumulative shocks over two years increases the probability of elevated blood pressure by 9.5%, increases waist circumference by 1.2% and the cholesterol ratio by 6.1% for those whose wealth is all in shares. My findings suggest that the combined effect of random shocks to financial wealth over time is salient for health outcomes. This is consistent with the allostatic load model in which repeated activation of stress responses leads to cumulative wear and tear on the body.

The UK equity release market: Views from the regulatory authorities, product providers and advisors

International Review of Financial Analysis, 2022

Tripti Sharma, Declan French, Donal McKillop

This study investigates the factors constraining the development of the UK equity release market. The results of a thematic review of interviews with industry stakeholders (product providers, advice providers and regulators) suggest that the attractiveness of the equity market for insurance companies (the main funders of the market), has diminished following a decline in annuity business and complications around the capital maturity matching requirements under Solvency II. Product costs (interest charges, and the cost of financial advice) are high. Trust in the market has improved, but remains fragile. Increased entry into the market by recognised brand names, (such as the traditional mortgage providers) would increase competition, reduce costs and promote trust. The risk of reputational damage limits the appeal of the market to new entrants. The no negative equity guarantee, a cost in terms of lower than otherwise loan-to-value ratios, promotes demand by way of the protection it affords to customers and their beneficiaries. Equity release is unsuitable for funding long-term care and policymakers advocating it as such damage the market.

HIV treatment and worker absenteeism: Quasi-experimental evidence from a large-scale health program in South Africa

Journal of Health Economics, 2021

Dominik Jockers, Sarah Langlotz, Declan French, Till Barnighausen

Over the past decade, large-scale HIV antiretroviral therapy (ART) programs have proven hugely successful in improving life expectancy for people living with HIV. However, the extent to which treatment allows patients to maintain a productive work life remains an open question. We apply an instrumental variable method based on individual CD4 counts and exogenously changing treatment guidelines to identify the causal effect size of ART on health-related absenteeism rates among workers living with HIV. We use monthly data from the occupational health program of one of the world’s largest mining companies in South Africa (128,052 observations among 1,924 workers, from 2009 to 2017). Eighteen months after HIV treatment initiation, antiretroviral therapy significantly reduces absenteeism by 1.033 days per worker and month. Using publicly available wage and treatment cost data, we find that the cost savings due to the absenteeism effect of ART alone outweigh treatment costs in the mining sector in several Sub-Saharan African countries.

Infographics by Topic