Banking

The role of ESG in shaping the impact of financial development on banks' performance

European Financial Management, 2025

Noman Arshed; Yassine Bakkar; Marco De Sisto; Mubasher Iqbal; Shajara Ul-Durar

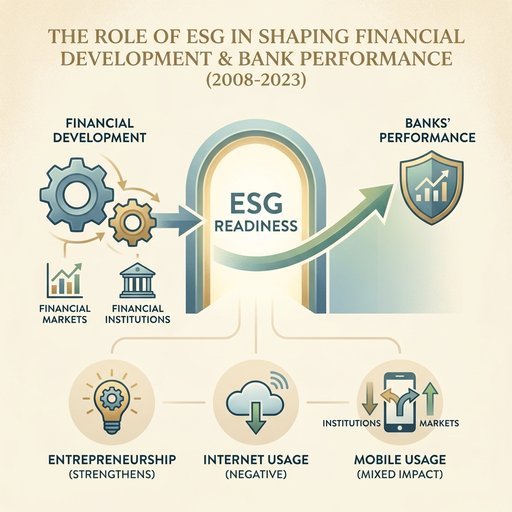

This study investigates how financial development, divided into financial markets and financial institutions, affects banks' performance across 93 financially developed countries during the period between 2008 and 2023. The analysis highlights the role of environmental, social and governance readiness as core determinants that reshape financial progress and banking outcomes. On the basis of financial intermediation theory and the broader idea of stakeholder engagement, this study finds that entrepreneurship strengthens bank performance, internet usage negatively affects it, and mobile usage shows a negative effect in the case of financial institutions but a positive impact when financial markets are considered.

Modeling and predicting failure in US credit unions

International Journal of Forecasting, 2024

Qiao (Olivia) Peng, Donal McKillop, Barry Quinn, Kailong Liu

This study presents a random forest (RF)-based machine learning model to predict the liquidation of US credit unions one year in advance. The model demonstrates impressive accuracy on the test set (97.9% accuracy, with 2.0% false negatives and 8.8% false positives) when utilizing all 44 factors. Simplifying the model to only the top five factors based on feature importance analysis results in a slightly lower, but still significant, accuracy on the test set (92.2% accuracy, with 7.8% false negatives and 17.6% false positives). Comparisons with seven other classification methods verify the superiority of the RF model. This study also uses the Cox proportional-hazards model and Shapley value-based approaches to interpret key feature significance and interactions. The model provides regulators and credit unions with a valuable early warning system for potential failures, enabling corrective measures or strategic mergers to ultimately protect the National Credit Union Share Insurance Fund.

Borrower- and lender-based macroprudential policies: What works best against bank systemic risk?

Journal of International Financial Markets Institutions and Money, 2022

Nicholas Apergis, Ahmet F. Aysan, Yassine Bakkar

This paper investigates the complementarity between the different macroprudential policies to contain bank systemic risk. We use a newly updated version of the IMF survey on Global Macroprudential Policy Instruments (GMPI). By disentangling the aggregate macroprudential policy index, we assess the complementarity between borrower-targeted and lender-targeted instruments in mitigating systemic risk arising from intra-financial system vulnerabilities. We investigate the effect of boom-bust cycle on such a relationship by analyzing the financial upturns and downturns and show the effectiveness of the macroprudential policies during calm period. We also show that their efficacy in mitigating instability is quite heterogeneous and may vary depending on the set of tools implemented, as well as bank size, TBTF, leverage, liquidity and concentration. Our results bear critical policy implications for implementing optimal macroprudential tools and provide insights into the trade-off between financial vis-a-vis price stability.

Bank Deregulation and Stock Price Crash Risk

Journal of Corporate Finance, 2022

Viet Anh Dang, Edward Lee, Yangke Liu, Cheng Zeng

This paper examines the influence of bank branch deregulation on corporate borrowers' stock price crash risk. Using a large sample of U.S. public firms over the period 1962-2001, we provide robust evidence that intrastate branch reform contributes to the reduction of firms' stock price crash risk. Further analysis shows that the negative relation between bank branch deregulation and crash risk is more pronounced among firms that are more dependent on external finance and lending relationships, as well as firms that have weaker corporate governance and greater financial constraints. Our findings are consistent with the notion that bank branch reform improves bank monitoring efficiency, thereby reducing borrowing firms' bad news formation and hoarding, and hence their stock price crash risk. Overall, our empirical evidence suggests that, as a reform aimed at removing restrictions on bank branch expansion, bank deregulation also helps protect shareholders' wealth.

How do institutional settings condition the effect of macroprudential policies on bank systemic risk?

Economics Letters, 2021

Nicholas Apergis, Ahmet F. Aysan, Yassine Bakkar

This paper investigates the impact of different country-traits of the effects of macroprudential policies on systemic risks in OECD countries. The analysis documents that institutional quality, high capital stringency, and moderate supervision support macroprudential policies in mitigating systemic risks, depending on macroprudential instruments in force. Institutional, regulatory and supervisory frameworks differently affect the effectiveness of lender--vis-a-vis borrower-targeted policies.

Internationalization, foreign complexity and systemic risk: Evidence from European banks

Journal of Financial Stability, 2021

Yassine Bakkar, Annick Pamen Nyola

Using a novel cross-European dataset on bank internationalization, the paper accounts for organizational and geographic complexity and evaluates its impact on systemic risk and how both the 2008-09 global financial crisis and the 2010-11 European sovereign debt crisis might have modified such an impact. Ahead of the crisis (2005-07), results suggest that bank complexity materially reduces systemic risk and enhances stability, as it encourages banks to take on more diversified risks. While such a relation is inverted during the crisis (2008-11) and after the crisis (2012-13), consistent with the view that, during distress times, international banks have less ability to monitor cross-border risks. Further evidence show that, regardless of the period, the effect of complexity on systemic risk is accentuated for 'too-big-too-fail' banks and banks with strong activity diversity. Conversely, complex banks with merger-acquisition history and banks operating networks of foreign branches mitigate systemic risk during the acute crisis and the later stage of the crisis, respectively. The results are robust to the use of alternative measures of systemic risk and complexity, and numerous additional tests. Findings bear critical policy implications for financial regulations.

Infographics by Topic