FinTech and AI

Do global COVOL and geopolitical risks affect clean energy prices? Evidence from explainable artificial intelligence models

Energy Economics, 2025

Sami Ben Jabeur, Yassine Bakkar, Oguzhan Cepni

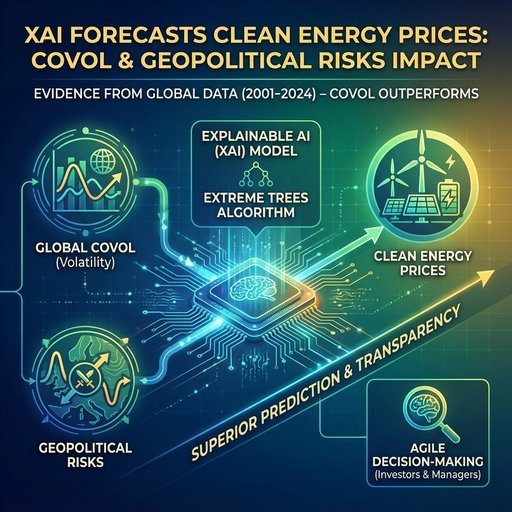

We investigate the impact of global common volatility and geopolitical risks on clean energy prices. Our study utilizes daily data from January 1, 2001, to March 18, 2024. Using a new framework based on explainable artificial intelligence (XAI) methods, our findings demonstrate that the COVOL index outperforms the geopolitical risk index in accurately predicting clean energy prices. Furthermore, the Extreme Trees algorithm shows superior performance compared to traditional regression techniques. Our findings indicate that XAI improves transparency, thereby making a substantial contribution to agile decision-making in predicting clean energy prices. Practitioners, including investors and portfolio managers, can enhance investment decisions and manage systemic risks by incorporating COVOL into their risk assessment and asset allocation models.

Mortality prediction using data from wearable activity trackers and individual characteristics: An explainable artificial intelligence approach

Expert Systems with Applications, 2025

Byron Graham, Mark Farrell

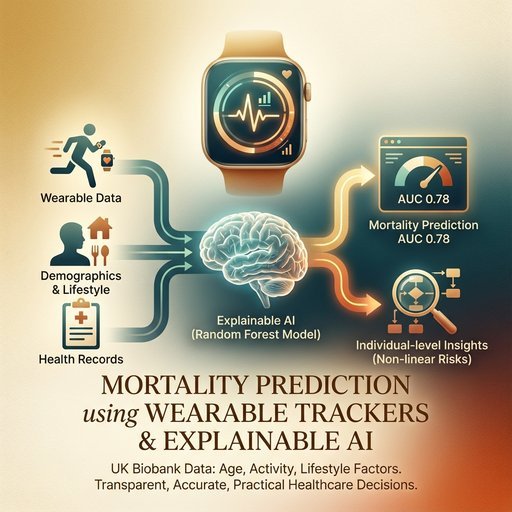

Mortality prediction plays a crucial role in healthcare by supporting informed decision-making for both public and personal health management. This study uses novel data sources such as wearable activity tracking devices, combined with explainable artificial intelligence methods, to enhance the accuracy and interpretability of mortality predictions. By using data from the UK Biobank—specifically wrist-worn accelerometer data, hospital records, and various demographic and lifestyle factors, and health-related factors—this research uncovers new insights into the predictors of mortality. Explainable artificial intelligence techniques are employed to make the models’ predictions more transparent and understandable, thereby improving their practical applications in healthcare decisions. Our analysis shows that random forest models achieve the highest prediction accuracy, with an area under the curve score of 0.78. Key predictors of mortality include age, physical activity levels captured by accelerometers, and other health and lifestyle factors. The study also identifies non-linear relationships between these predictors and mortality, and provides detailed explanations for individual-level predictions, offering deeper insights into risk factors.

Evolutionary multi-objective optimisation for large-scale portfolio selection with both random and uncertain returns

IEEE Transactions on Evolutionary Computation, 2024

Weilong Liu, Yong Zhang, Kailong Liu, Barry Quinn, Xingyu Yang, Qiao Peng

With the advent of Big Data, managing large-scale portfolios of thousands of securities is one of the most challenging tasks in the asset management industry. This study uses an evolutionary multi-objective technique to solve large-scale portfolio optimisation problems with both long-term listed and newly listed securities. The future returns of long-term listed securities are defined as random variables whose probability distributions are estimated based on sufficient historical data, while the returns of newly listed securities are defined as uncertain variables whose uncertainty distributions are estimated based on expert knowledge. Our approach defines security returns as theoretically uncertain random variables and proposes a three-moment optimisation model with practical trading constraints. In this study, a framework for applying arbitrary multi-objective evolutionary algorithms to portfolio optimisation is established, and a novel evolutionary algorithm based on large-scale optimisation techniques is developed to solve the proposed model. The experimental results show that the proposed algorithm outperforms state-of-the-art evolutionary algorithms in large-scale portfolio optimisation.

Going mainstream: cryptocurrency narratives in newspapers

International Review of Financial Analysis, 2024

Clive B. Walker

This paper quantifies mainstream media coverage of Bitcoin to understand how a once niche interest entered public culture. From 2011 to 2022, five key narratives are identified as criminality, culture, politics, price and technology. Price, politics, and culture have become more prominent in coverage while the technology narrative has waned. Coverage that is more political or cultural is associated with subsequently lower returns whereas the criminality narrative is associated with higher returns. Together this suggests that as narratives have become more mainstream, they have created additional demand, despite the negative association with criminal activity.

Practice-relevant model validation: Distributional parameter risk analysis in financial model risk management

Annals of Operations Research, 2023

Mark Cummins, Fabian Gogolin, Fearghal Kearney, Greg Kiely, Bernard Murphy

An objective of model validation within organisations is to provide guidance on model selection decisions that balance the operational effectiveness and structural complexity of competing models. We consider a practice-relevant model validation scenario where a financial quantitative analysis team seeks to decide between incumbent and alternative models on the basis of parameter risk. We devise a model risk management methodology that gives a meaningful distributional assessment of parameter risk in a setting where market calibration and historical estimation procedures must be jointly applied. Such a scenario is typically driven by data constraints that preclude market calibration only. We demonstrate our proposed methodology in a natural gas storage modelling context, where model usage is necessary to support profit and loss reporting, and to inform trading and hedging strategy. We leverage our distributional parameter risk approach to devise an accessible technique to support model selection decisions.

Infographics by Topic